Understanding the taxation of rental schemes in Lyon

Lyon's rental investment market is attracting more and more property owners in search of profitability and asset security. But, more than ever, landlords have to navigate a complex tax landscape, marked by recent reforms and increasingly precise regulations. In this context, choosing the right tax regime can quickly become a headache.

Whether you choose to rent bare property, rent furnished non-professionally (LMNP), rent furnished professionally (LMP) or rent seasonally, each regime has its own advantages, constraints and major tax implications. We take a look at the different tax regimes to help you make the right choice for your situation.

Bare-rental: simplicity at the cost of heavier taxation

Bare-rental, i.e. a property offered for unfurnished rental as a principal residence, remains a classic formula. For tax purposes, rental income is taxed as “revenu foncier”.

There are two types of regime for unfurnished rentals:

The micro-foncier system

If annual rental income does not exceed €15,000, the tax system corresponds to the micro-foncier system. This provides a flat-rate deduction of 30%, with no need to justify expenses.

Real estate regime

If annual property income exceeds €15,000, the tax regime is the real estate regime. Under this system, actual expenses incurred in managing the property can be deducted, including loan interest, maintenance and/or renovation work, property tax, management and insurance fees, etc.

Good to know: Whether you use the micro-foncier system or the real-estate system, there are no accounting requirements for bare-rental properties.

In short, bare rental offers the advantage of simplicity, but profitability is often low, with few levers for optimization.

The major drawback? The impossibility of recognizing a deficit that can be deducted from overall income, except within certain limits (property deficits can only be deducted from overall income up to a limit of €10,700 per year, and only if loan interest is excluded). What's more, tax rates can quickly escalate with income tax (up to 45%) and social security contributions (17.2%).

All in all, the tax burden on rental income can be high, especially for taxpayers in a high marginal tax bracket. On resale, the property is subject to the capital gains tax system for private individuals, with the application of deductions for the length of time the property has been held.

Furnished rental: a more favorable tax framework

Furnished rental is an increasingly popular alternative in Lyon, with fully-equipped properties that enable tenants to move in immediately. A property is considered furnished when it includes the furniture required for normal daily living: bed, table, chairs, crockery, refrigerator, hotplates, etc.

For tax purposes, furnished rentals come under the industrial and commercial profits regime (BIC), which opens the way to a number of optimization levers.

There are two types of status:

Non-professional furnished rental (LMNP)

LMNP is available if annual rental income does not exceed €23,000, or if it represents less than 50% of the professional income of the tax household.

There are two tax options for LMNPs:

Micro-BIC: which applies a deduction of 50% (or 30% for unclassified furnished accommodation). Simple to manage, it requires no complex bookkeeping;

The “régime réel”: much more attractive in most cases. This allows you to deduct all expenses, as well as depreciate the property (excluding land) and furniture. In this way, a large proportion of the rent received can be neutralized for tax purposes. However, the “régime réel” system requires you to keep accounts and declare annual income.

Professional furnished rental (LMP)

To qualify for LMP status, rental income must exceed €23,000, and rental income must represent more than 50% of the professional income of the tax household.

This status gives access to an ultra-optimized regime with even greater advantages. In addition to depreciation and deduction of expenses, the lessor can be exempted from the Impôt sur la Fortune Immobilière (IFI) tax on real estate wealth if the business is carried on as a principal activity. In the event of resale, capital gains may be fully or partially exempt, depending on the length of time the business has been in operation and the level of revenue.

It should be noted, however, that this status requires proper accounting, with registration in the trade register and specific declarations.

CAUTION: since January 2025, depreciation taken during the holding period must be added back when calculating the taxable capital gain in the event of resale. This automatically reduces the tax benefits of the real-estate system, particularly for long-term investors.

Seasonal rental: between high profitability and complexity

Seasonal rental is defined as short-term rental (Airbnb, tourist residence, chambre d'hôte...), often intended for stays of a few days to a few weeks.

Very much in vogue via platforms like Airbnb, it can offer exceptional profitability, especially in Lyon's prized neighborhoods (such as Vieux Lyon, Tête d'Or, Croix-Rousse, Bellecour, Confluence, etc.). However, this type of rental is now subject to strict regulations.

From a tax point of view, it is treated as a commercial activity, and comes under the BIC regime. If revenues are less than €77,700, the lessor can opt for the micro-BIC system, with a deduction of 50% for classified or unclassified furnished tourist accommodation, and 30% for standard residential rentals. Otherwise, you can deduct expenses and depreciate the property under the “régime réel”.

Please note, however, that as soon as the lessor offers at least three para-hotel services (breakfast, cleaning, linen supply, reception), the rental becomes subject to VAT. This entails more complex management, but in some cases also enables VAT to be reclaimed on works, furniture or acquisitions.

Other constraints to be aware of: the application of the CFE (Cotisation Foncière des Entreprises), the possible surcharge of the taxe d'habitation on second homes, and local town-planning regulations, particularly in Lyon, where specific authorizations are required to transform a property into a furnished tourist accommodation.

Important note: The city of Lyon now regulates this type of rental, both in terms of administrative authorizations and condominium regulations. Please do not hesitate to contact us for further information...

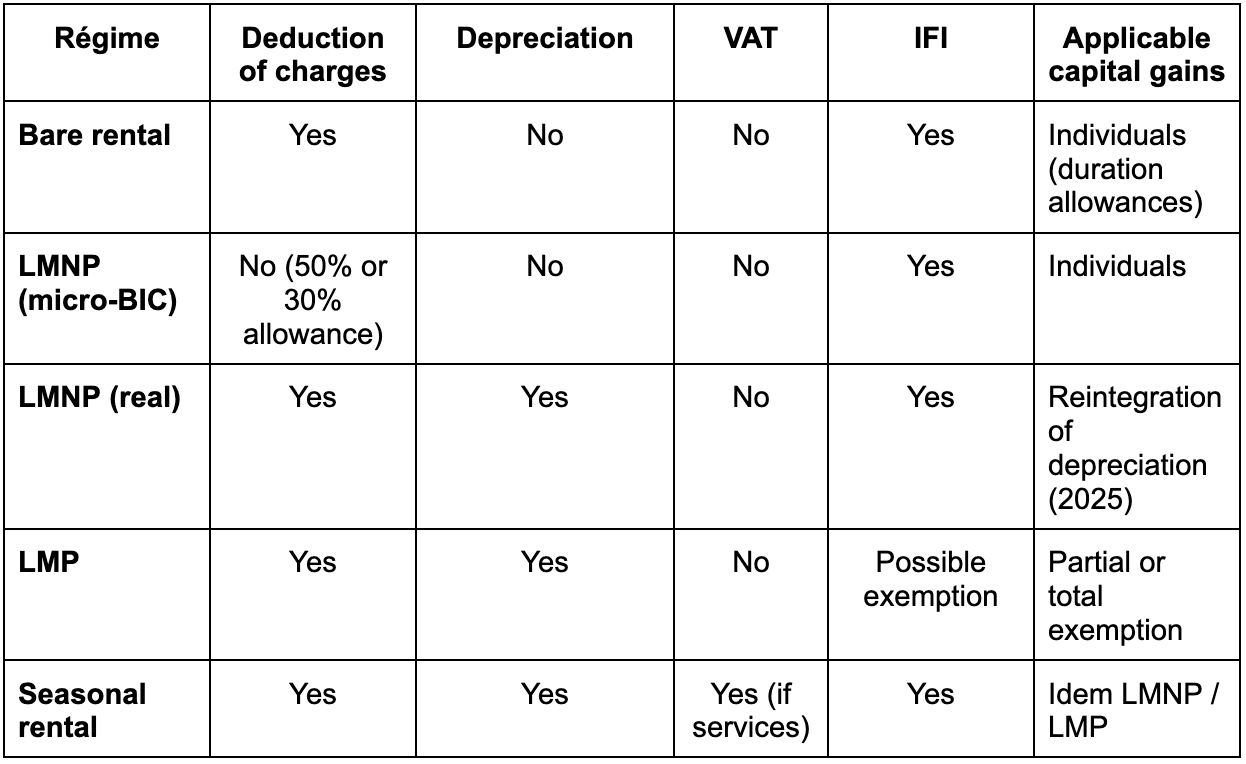

Comparison of different rental regimes

Here's a summary table to help you visualize the main differences between the tax regimes applicable to rental :

Renting a property in Lyon: why choose Barnes Lyon?

Faced with the growing complexity of tax regimes and constantly evolving legislation, it's essential to benefit from tailor-made support. At BARNES Lyon, we put at your disposal a team of specialists in rental management, taxation and wealth strategy.

Thanks to our experts, we can help you :

Analyze your project and choose the tax system best suited to your situation;

Rent out your property in a professional manner;

Monitor your rental management on a daily basis, with rigor and transparency;

Optimize your profitability according to the property, your profile and your objectives, while securing your investment over the long term;

Whether you own a family apartment in the 6th arrondissement, a pied-à-terre in Vieux Lyon or a second home in the west of Lyon, we have the solutions to suit your profile and ambitions.

Contact Eva Châtel, Rental Manager at BARNES Lyon, for a personalized study of your rental project in Lyon.